17th February 2021

The Fall Of Arcadia: A Digital Oversight

In recent news, online fashion retailer ASOS has bought the Topshop, Topman and Miss Selfridge brands from failed retail group Arcadia in a deal worth £295m.

Widely renowned for its prominent store locations, the cluster of brands under the Arcadia group’s umbrella have dominated our high streets and shopping centres for many years. With many familiar names, Arcadia’s collection of brands included: Burton, Dorothy Perkins, Evans, Miss Selfridge, Outfit, Topman, Topshop and Wallis. But why have ASOS only bought Topshop, Topman and Miss Selfridge brands?

Operating online-only, it makes sense that ASOS have acquired the stocks and brands, but not the physical stores. ASOS CEO Nick Beighton commented:

"The acquisition of these iconic British brands is a hugely exciting moment for ASOS and our customers and will help accelerate our multi-brand platform strategy.”

"We have been central to driving their recent growth online and, under our ownership, we will develop them further, using our design, marketing, technology and logistics expertise, and working closely with key strategic retail partners in the UK and around the world."

"We think we're the natural owners for these brands. We know these customers and we know this market.” ASOS also added that the brands would benefit from "investment into customer engagement and brand positioning in line with our existing model".

Whilst there is no doubt that the hard-hitting impacts of COVID-19 were clear and major contributing factors to the downfall of the group, it is thought that many issues pre-dated the pandemic. Julie Palmer of Begbies Traynor said: "While the COVID-19 crisis has undoubtedly accelerated the company's decline, in reality, the writing had been on the wall for Arcadia for some time. Its competitors forged ahead with high-profile online propositions that it simply failed to match."

What Went Wrong?

Described as “more of a yesterday’s man than he is a tomorrow’s man”, it could be said that the criticism levelled at Sir Phillip Green in 2015 has now (with the recent failure of Arcadia) proven to have some substance.

Falling into administration in November 2020, Arcadia had been struggling to keep pace against newer, online-only fashion retailers such as ASOS, Boohoo and Pretty Little Thing for some time. Not to mention the added pressure from traditional high-street competitors such as Zara and H&M operating very successfully in the online space too. So what went wrong? We’ll explore below.

The evolving UK fashion market

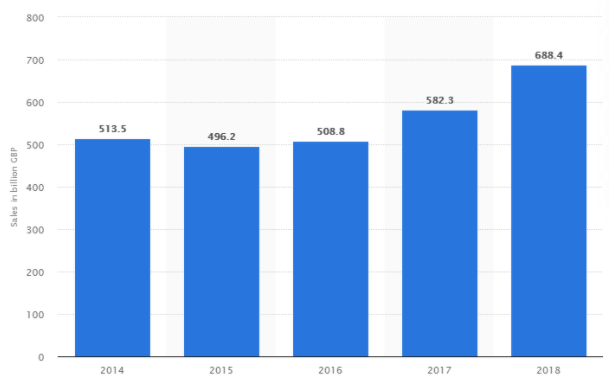

The UK fashion market is well-known for its dynamic and fast-paced nature, with trends, styles and fits rapidly changing. With the most advanced ecommerce market in Europe, the graph below illustrates the growth in ecommerce sales pre-COVID-19.

Image

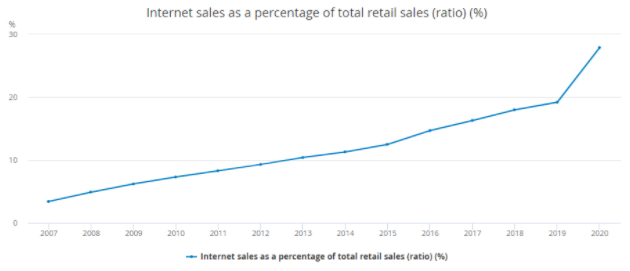

The UK’s ecommerce revenue in 2018 amounted to £688.4 billion, which was a sharp increase on 2017. The Office For National Statistics (UK) graph below shows internet sales as a percentage of total retail sales were at 18% in 2018, 19.2% in 2019 and then rapidly rose to 27.9% in 2020. eMarketer forecasts this trend to continue, with ecommerce sales to account for a third of all retail sales by 2024.

Image

Digital buying took hold of the nation as the COVID-19 pandemic decimated the high street during 2020. Undoubtedly, the pandemic expedited a move to UK consumers shopping digitally, with online ordering becoming a necessity for acquiring any non-essential items during lockdown. Compared to 2019, clothing stores recorded a -25.1% annual decline in sales volumes in 2020. Non-store retailing, however, saw a record annual increase of 32% for 2020.

In line with the decline of the high street and the increase in personal accessibility and usage of smart devices, new exclusively ecommerce competitors have been successfully penetrating the UK fashion market, with comprehensive digital marketing strategies at the core of their successful business models.

Tamara Sender, Retail Analyst at Mintel explains:

“Appetite for clothing has dropped dramatically since the first lockdown and will be dealt a further blow with the second national lockdown during peak trading season, making it one of the hardest-hit retail sectors in 2020. As online shopping for fashion increases and the shift away from stores creates a longer-lasting legacy, this will accelerate the pace of digitisation of the clothing retail sector. Retailers that are able to be agile and flexible in order to adapt to the new reality are most likely to succeed.”

It’s clear that as traditional fashion retailers look to increase their online presence, search marketing is integral to their success. It can be argued that the Arcadia Group as a whole was not agile or flexible enough to adapt at pace during a period of accelerated market pressures. Not making fundamental digital transformation to stop ecommerce-only brands dominating the online fashion space, they struggled and ultimately paid the price.

Bricks and mortar restraint

Traditional high-street retailers suffer from rising business costs, inflating wage bills and long-term, sometimes unsustainable lease agreements. This, coupled with the decline of high streets in general, reduced overall footfall. Add to that, almost ten years of austerity has put real pressure on retailers operating from physical locations.

Stock sitting in stores is not as easy to fulfil as online orders being picked and packed from a central warehouse. Making the transition to a business with more of a core digital offering is likely to be logistically challenging, costly and a huge undertaking with the restructuring of the business and its stakeholders. Companies who have hastened this transformation and reduced the shackles of their physical stores have started to hold their own against the more progressive online-only retailers. Unfortunately, the Arcadia group did not manage to do this across their portfolio of brands.

So could Arcadia ever compete with ecommerce-only brands? As well as almost ten years of austerity, Richard Lim, an analyst at Retail Economics, suggested the rise of online shopping has also been a key factor in Arcadia’s troubles, saying "Not only are retailers facing fixed costs they face huge costs fulfilling online orders. That's a lot easier to handle if you are a smaller, nimbler operator." - which many pure ecommerce competitors are, and Arcadia certainly is not.

Changing consumer demands

Even pre-COVID-19, throughout the last decade consumers have become more curious, demanding and impatient. Thanks heavily to the emergence of smart mobile devices, we’ve seen a general paradigm shift towards online shopping. The recent effects of a pandemic, with consumers spending a large part of 2020 in lockdown, have simply accelerated a consumer move to shopping online with a huge surge seen in 2020.

This transition in consumer expectations has pushed companies to adopt far more robust inventory management, ordering and fulfilment protocols. Companies now offer same or next day delivery for free or at very low prices, with some now offering robot deliveries in more urban areas, too. More forward-thinking companies such as ASOS offer consumers more freedom, by offering unlimited next-day delivery and free returns for only £9.95 a year.

Image

A failure to appreciate these changing consumer demands, react quickly and implement wide-scale operational changes can be catastrophic. In the case of Arcadia, with so many differing sub-brands, this was always going to be an uphill battle. Each sub-brand, with varying and ageing consumer demographics, (some less profitable than others) as well as location-specific, poor-performing stores, ultimately stretched the group as a whole.

This is illustrated further by the fact ASOS chose only to purchase certain brands, which were a better fit with their online offering and consumer base. ASOS's mission is to become "the number one destination for fashion-loving 20-somethings throughout the world". This target audience is widely-known to be more digitally savvy and comfortable shopping online, and this arguably intimates that ASOS chose these brands due to their potential to further thrive as part of an ecommerce business.

David Beadle, vice president at credit rating agency Moody’s, proposed that heavy discounting has added to Arcadia Group’s challenges, with the group being the latest in a long line of once strong clothing retailers to struggle to keep up with consumers’ insatiable desire for newness, value, convenience and engagement.

Forward-thinking businesses have aligned themselves with changing consumer demands by becoming body-inclusive, using plus-sized models and understanding the substantial impact that influencers have on shopping habits, using them to the detriment of competitors who have not.

Fast fashion, price and sustainability

In recent years, fast fashion competition has heated up drastically. Brands such as Bohoo have managed to offer dirt-cheap fashion, whilst remaining on-trend, reacting to changing fashion requirements almost instantly. This ability to turn around new collections and styles at pace - coupled with other benefits associated with being an ecommerce business, such as the ability to sell surplus warehouse stock easily with flash online sales - makes them extremely lean and efficient businesses.

Younger consumers are becoming increasingly aware of the impact of their purchases and the brands they choose to interact with. Pressure is now on brands to improve their sustainability reputations as these consumers move into higher-earning roles.

Research on UK and US internet users from GlobalWebIndex shows:

- 68% of online consumers would or might stop using a brand because of poor or misleading CSR.

- 84% say a poor environmental track record would or might cause them to stop buying from a brand.

- Nearly half are willing to pay a premium for socially-conscious or environmentally-friendly brands.

With sustainability becoming more regularly on consumer’s minds when purchasing, it’s something that retailers are being pushed to take more seriously. This affects the fast fashion businesses in particular, where it can be argued that it’s generally more difficult for them to operate in a completely sustainable and ethical manner whilst trading at such low and competitive price ranges.

The emergence of the more ethically motivated consumer means an added factor to the consideration phase of a purchase. Consumers may be willing to pay slightly more to purchase from a company with morals more closely aligned with their own, but will they pay more for an item simply because there is the option to see it in person at a physical store? The answer is, it’s unlikely. An article by Grazia Daily reiterates this. Shoppers were asked why they stopped shopping at Topshop, one of Arcadia’s most prominent brands. Some notable consumer feedback was:

“Nowadays, I would avoid fast fashion because I understand the impact cheap prices have on workers, but Topshop was more expensive and just as unethical as the other fast fashion brands. If they’d have gone sustainable I think that would’ve encouraged me to go back, but without reinventing the brand there was no justification for the prices they charged.”

On the whole, Arcadia’s brands offered an equally unsustainable option as its fast fashion competitors, but at a higher price point, whilst also having its collections somewhat tied to traditional season based collections due to the physical location of their stock.

Lack of omnichannel strategy

With the growth of fast fashion, the age of Instagram and changing consumer behaviour, the acceleration of digital commerce and prominence of social commerce are channels that businesses can ill-afford to overlook.

Once at the forefront of innovation in retail, Arcadia failed to embrace an omnichannel approach across their full portfolio of brands. A lack of timely investment and focus in areas where their consumers were transitioning to, or had already long migrated to, meant an outdated perspective of the fashion retail market. Now encompassing a far more fragmented customer journey, it requires an in-depth understanding of the multiple touchpoints and consideration phases when advertising to and engaging with target consumers.

This delay in investment allowed new fast fashion entrants such as PrettyLittleThing, along with their powerful customer engagement strategies, to storm the market. Powered by social commerce and geared towards a young demographic of women, the brand captured a changing, progressive and digitally savvy market. Traditional department stores who were slow to move to an omnichannel strategy and continued to deal with their channels as individual silos will have experienced a lag in sales. This will have been further exacerbated by market disruptors eating up a share of the market.

Being a driving force for retail over the past few decades was not enough, and neither was simply selling online what you already sold in store. This was a problem for Arcadia. Endless creativity and adaptability in the face of adversity is what will pull businesses through hard times like the COVID-19 pandemic. Today’s most successful brands have a creative function at the heart of their business, with a vision which encapsulates the need for their consumers to feel part of the brand - buying into, rather than mindlessly buying from.

Conclusion

Ultimately, an evolving market, increased competition, a lack of omnichannel strategy and changing consumer demands all played their part in the fall of Arcadia, but it was COVID-19 which fired the final nail into the coffin of the retail giant.

The digital landscape was not an enemy of the Arcadia group. A failure to innovate and show creativity in the digital space within a rapidly advancing market made it difficult to compete. Combine this with the pressures imposed on the market from new fast fashion, market-disrupting ecommerce retailers and the landscape becomes even more difficult to navigate. Arcadia struggled to bridge the online gap in a market where having a thorough and enterprising ecommerce capability was a must, whilst physical stores became more of a financial and operational constraint, rather than an effective differentiator.

The rise in online shopping could have been an opportunity for them to exploit, but a lack of definitive action left them in the wake of more critically decisive traditional competitors. The group clearly had deep-rooted issues pre-COVID-19 and the pandemic simply exaggerated the issues and put further tension on the business. The chastity belt caused by physical stores meant they had restraints when it came to investing in the digital futureproofing of their business. An overall digital oversight was further highlighted by the effects of COVID-19 and illustrated a growing disparity between how traditional high street retailers and exclusively ecommerce stores operate.

Free eBook For Online Retailers

Download our Navigating the Biggest Challenges for Online Retailers eBook now for insights into AI and Machine Learning, Personalisation, Automation, Voice Search, Big Data and more.

x